Written by Dr. Robert Rifkin | Sponsored by Mylan Pharmaceuticals

Biologic agents have long played a vital role in oncology. Not only does this class of agents represent the best of science, but it also accounts for a tremendous increase in spend of the healthcare dollar. As the field of biologic therapies advances, the biosimilarity exercise has become relevant. The premise of biosimilarity is to decrease healthcare costs and improve access to care.1

This premise was first established with the affordable care act in the Biologics Price Competition and Innovation Act (BCPIA).2 Since its inception, a new pathway for approval of biosimilars was tested and implemented. The 351 (K) regulatory pathway was first tested with biosimilar filgrastim (filgrastim–sndz), or Zarxio.3 Initially, upon product launch, a modest discount of 15% was employed. (15%) The uptake was slow; however, when the market adjusted and uptake accelerated, an approximate 30% discount was in play.

Several other biosimilars have now entered the supportive care space. Specifically, in the case of short acting filgrastim, there are now competitors Nivestym (Filgrastim-aafi) with several additional biosimilar filgrastims under development. Within the pegfilgrastim arena, the position of the originator, Neulasta, has now been challenged by 3 other long-acting filgrastims: Fulphila (pegfilgrastim-jmdb), Udenyca (pegfilgrastim-cbqv), and Ziextenzo (pegfilgrastim-bmez).4 These original, early supportive care biosimilars have helped to define the marketplace, test regulatory mechanisms, and dispel any myths regarding their adoption.4

Herceptin (trastuzumab) also faces competition as new biosimilars enter space. Multiple biosimilars have now launched in addition to the originator molecule, including: Herzuma (trastuzumab-pkrb), Kanjinti (trastuzumab-anns), Ogivri (trastuzumab-dkst), Ontruzant (trastuzumab-dttb), and Trazimera (trastuzumab-qyyp).5 For the trastuzumabs, the large number of biosimilar options provides both competition in the marketplace in addition to a potential new source of significant confusion with distribution, supply chain, and inventory management. It is relatively unlikely that any payor or formulary will carry all five biosimilar trastuzumabs currently available in addition to any other biosimilar options slated for release over the next year.

Additionally, the rituximab space has become increasingly complex. Beyond the originator molecule, we can now choice to use Truxima (ritiximab abbs), or Ruxience (rituximab-pvvr), and several more launches are anticipated. The space is further complicated by the availability of a subcutaneous form of Rituxan Hycela (rituximab/hyaluronidase human), the only biosimilar available in subcutaneous injection. Unsurprisingly, this has created some from payors as all labeled indications are not initially the same for each product. Moving forward, rituximab biosimilar labels will soon be equivalent, and competition will then drive the marketplace.

In the real world, there still exist very real barriers to adoption including a clinical, ease of use, and economic barriers. It is likely payors will interpose themselves into each one of these. Multiple biosimilars are now being approved for each originator molecule. This will ultimately result in a decline in cost. Payors and other stakeholders will then be faced with complicated decisions of maintaining the originator on the formulary, deleting it and placing a biosimilar in its place, or perhaps carrying two versions of the same molecule, with preference being given to one. Most likely, most formularies will carry originator in addition to one or more biosimilars concurrently depending on the provider and payer landscape. the originator and a preferred biosimilar concurrently.

Several articles have reviewed the concept of switching between the biosimilar and the originator, and to date no significant safety signals have arisen.6 The payor landscape is impacted by product availability and opportunities to switch. This demonstrated safety of switching has incrementally impacted the payor landscape. Pharmacy Benefit Managers (PBM) have also been interwoven into the payor conundrum, with discounts and rebates providing an additional layer of complexity.

Not only is the transition to biosimilars complicated for payors, but the transition must also include all stakeholders involved in the ultimate selection of a therapeutic biologic. Providers and patients need to be very well educated regarding the concept of biosimilarity. Other stakeholders, including pharmacists, advanced practice providers, nurses, and admixture technologists, must be thoroughly educated. The electronic health record also needs to be updated to reflect the increasing numbers of biosimilars now available – including the preferred therapeutic agents in each circumstance.

Payors and clinicians alike will need to develop biosimilar teams, drug contracting strategies with and without GPO’s, and a thorough evaluation of clinical economics for each biosimilar. Biosimilars will assume an increasingly important role in the delivery of cancer care and it is important to approach this from a patient journey point of view (Fig. 1).

Figure 1: Patient Journey7

By tracing this from beginning to end, a formula for success may be developed.

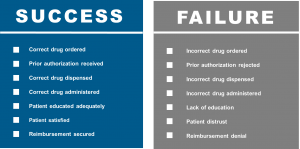

The combination of clinical confidence, patient confidence, and operational excellence will be required to be sure that we are prepared for biosimilars and ensure patient access. The patient’s journey is complicated and increasingly influenced by the payor and other stakeholders . Providers, consideration of the revenue cycle, RN educators, pharmacists, admixture technologists, and infusion RNs all must play together to ensure the success of biosimilars. In alignment with the patient journey, diagnosis and treatment selection will be accomplished by the provider. This will be followed by insurance authorization, treatment education, treatment scheduling, treatment admixture, and finally the delivery of the drug to the well-educated patient. There are many potentials for success as well as failure (Fig. 2).

Figure 2: Drug Preparedness – Success vs. Failure7

The cornerstone for all to succeed, as well as all of the affected stakeholders managing paired challenges, remains education. This cannot be overstated. Numerous websites have now appeared, both branded and unbranded, to help deliver biosimilar education. Such websites may be found at the FDA8 and the Center for Biosimilars.9

In conclusion, as all the stakeholders become thoroughly educated, the many challenges outlined above will continue to present themselves in real-time. The success and adoption of current and future biosimilars will continue to depend on the sound education of all stakeholders, including payors, in addition to improved cost savings and access. Biosimilar usage will be important to ensure long-term sustainability on the market, and as biosimilar uptake increases, healthcare cost reduction and improvements to care access may be achieved.

Sources

1. Pittman WL, Wern C, Glode AE. Review of Biosimilars and Their Potential Use in Oncology Treatment and Supportive Care in the United States.

2. https://www.fda.gov/media/78946/download

3. U.S. Food & Drug Administration. Zarxio (filgrastim-sndz) Approval Letter. Published online March 6, 2015. Accessed June 19, 2020. https://www.accessdata.fda.gov/drugsatfda_docs/nda/2015/125553Orig1s000Approv.pdf

4. Rugo H, Rifkin RM, Deckerc P, Bair AH, Morgan G. Demystifying Biosimilars: Development, Regulation and Clinical Use. Future Oncology. 15(7):777-790, 2019

5. AmerisourceBergen. Approval and launch dates for US biosimilars. Published June 19, 2020. Accessed June 25, 2020. http://gabionline.net/Reports/Approval-and-launch-dates-for-US-biosimilars?ct=t%28GONL+V20F19-6%29&mc_cid=2821e641cc&mc_eid=%5BUNIQID%5D

6. Cohen HP, Blauvelt A, Rifkin RM, Danese S, Gokhale SB, Woollett G. Switching Reference Medications to Biosimilars: A Systematic Literature Review of Clinical Outcomes. Drugs 78(4): 463-78,2018.

7. Rifkin R, Busby L. Bringing Biosimilars to Community. Presented at McKesson Oncology University; 2019.

8. www.fda.gov

9. www.centerforbiosimilars.com/